A Complete Guide to SHGs

[vc_row full_width=”stretch_row” content_placement=”middle” css=”.vc_custom_1504764629511{background-color: #002e5b !important;}” el_id=”panel_header”][vc_column][vc_row_inner][vc_column_inner][vc_column_text el_class=”chapter_head”]

A Complete Guide to SHGs

Author: Shivasankari Bhuvaneswaran

[/vc_column_text][/vc_column_inner][/vc_row_inner][vc_row_inner][vc_column_inner width=”2/3″][vc_empty_space][vc_column_text el_class=”header_text”]Most of us have heard about the SHG model in passing, and a few even get an opportunity to see their interaction on a day-to-day basis.

Despite all these, when faced with a question “how well do we really know SHGs?” it is sad to see that majority of us don’t seem to have a clue about the mere basics like what they do or how they work.

The lack of awareness is rather astounding. The reason behind this might be the abrupt dismissal of the concept by envisioning it as just ‘group of women who save and get a loan.’

Not many desire to delve deeper into how SHGs are contributing to poverty alleviation through women empowerment. A very few are ready to look beyond the concept of empowering rural women.

This blog intends to shed some light on the resilient revolutionary movement called SHG which is causing several drastic changes in the social and economic realms of our nation. [/vc_column_text][/vc_column_inner][vc_column_inner width=”1/3″][vc_empty_space][vc_single_image image=”7200″ img_size=”large” alignment=”center”][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row el_id=”chapters”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading source=”” text=”Contents” link=”” font_container=”tag:h2|text_align:center” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:600%20bold%20regular%3A600%3Anormal” el_class=”” css=”” icon=”” icon_size=”” subtitle=””][/vc_column_inner][/vc_row_inner][vc_row_inner][vc_column_inner width=”1/4″][vc_column_text]

Chapter 1

Chapter 1

[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/4″][vc_column_text]

Chapter 2

Chapter 2

[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/4″][vc_column_text]

Chapter 3

Chapter 3

[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/4″][vc_column_text]

Chapter 4

Chapter 4

[/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space height=”30px”][vc_row_inner][vc_column_inner width=”1/4″][vc_column_text]

Chapter 5

Chapter 5

[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/4″][vc_column_text]

Chapter 6

Chapter 6

[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/4″][vc_column_text]

Chapter 7

Chapter 7

Role of Promotional Institutions

[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/4″][vc_column_text]

Chapter 8

Chapter 8

[/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space height=”30px”][vc_row_inner][vc_column_inner width=”1/4″][vc_column_text]

Chapter 9

Chapter 9

Long term Socio-Economic Impact of SHGs

[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/4″][vc_column_text]

Chapter 10

Chapter 10

[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/4″][vc_column_text]

Chapter 11

Chapter 11

[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/4″][vc_column_text]

Chapter 12

Chapter 12

[/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row][vc_row full_width=”stretch_row” el_id=”chapter1″ css=”.vc_custom_1504719048892{background-color: #002e4b !important;}”][vc_column][vc_custom_heading source=”” text=”Chapter 1:

What are SHGs?” link=”” font_container=”tag:h1|text_align:center|color:%23ffffff” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:300%20light%20regular%3A300%3Anormal” el_class=”chapter_head” css=”” icon=”” icon_size=”” subtitle=””][vc_empty_space height=”16px”][vc_column_text]SHGs or Self-Help Groups are exclusive groups started primarily to empower women in rural and suburban areas, make them economically independent and help them contribute to the socio-economic development of the nation.

How do they achieve it? How long has this concept been around? Let’s delve a bit deeper to learn more about them.[/vc_column_text][vc_empty_space height=”15px”][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]SHGs or Self-Help Groups are exclusive groups started primarily to empower women in rural and suburban areas, make them economically independent and help them contribute to the socio-economic development of the nation.

Initially, all self-help groups focus on cultivating a strong saving habit amongst its members by making them deposit a little portion of their daily income in a kitty so that in case a member needs money immediately to tackle a personal issue, these savings could be offered to them as an internal loan to be repaid at a fixed interest within a stipulated time.

Over the last 20 years, the SHG groups which were started as a savings group has evolved into a social movement that has taken up the role of a livelihood promoter. This program has revolutionized the lives of women in the rural areas who have been oppressed within the confines of their home for far too long in a male-chauvinistic, patriarchal society.[/vc_column_text][vc_row_inner][vc_column_inner width=”2/3″][vc_column_text]

Source: TheNewsHimachal

Source: TheNewsHimachal

[/vc_column_text][vc_empty_space height=”8px”][/vc_column_inner][vc_column_inner width=”1/3″][vc_empty_space height=”48px”][vc_column_text]

Women not only constitute a major portion of poor, but they are also underemployed, discriminated, and disadvantaged both economically and socially.

[/vc_column_text][vc_empty_space][/vc_column_inner][/vc_row_inner][vc_column_text]The SHGs focus on women with the confidence that extending credit to women could create a change in a more rapid way. They are formed with the intention to given these women confidence and the skills to form, manage and build a sustainable community to take care of their livelihoods and grow holistically.

Several studies on male and female borrowers depict that when women get extra money, they tend to utilize it for the betterment of their family and children whereas men spend it lavishly on themselves. Hence, offering loans to women and empowering them with adequate training would directly influence the welfare of both children and men in the society. [/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]

[/vc_column_text][vc_empty_space][/vc_column][/vc_row][vc_row full_width=”stretch_row” el_id=”chapter2″ css=”.vc_custom_1504721001624{background-color: #002e4b !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading source=”” text=”Chapter 2:

Rise of SHG Movement” link=”” font_container=”tag:h1|text_align:center|color:%23ffffff” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:300%20light%20regular%3A300%3Anormal” el_class=”chapter_head” css=”” icon=”” icon_size=”” subtitle=””][/vc_column_inner][/vc_row_inner][vc_empty_space height=”16px”][vc_column_text]Now that we have little idea as to what they are, aren’t you a tad bit curious about the origin of such a revolutionary idea? Laying it a bit thick am I? But hey, just look at it this way.

Read in a dramatic voice: “In an era of oppression, helping the women form groups which offered them financial autonomy, tuned in their leadership skills and prepared them ready to handle social issues with confidence is a radical move.”

What made the authorities & the government take such an unprecedented action? Dramatics aside, let’s see what sparked this ingenious idea.[/vc_column_text][vc_empty_space height=”16px”][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_row_inner][vc_column_inner width=”2/3″][vc_empty_space height=”16px”][vc_column_text]While there has been lots of controversy regarding the origination of Self Help Groups, the majority of the folks seem to agree that the microfinance movement played a huge role in it.

Prof. Muhammad Yunus, the famed economist of Bangladesh, started the microfinance movement with a profound vision of eradicating poverty from the world by promoting women empowerment. Being a founder of the Grameen Bank, even today he is hailed widely as the “Father of Microfinance Industry.”

Before we learn more about Grameen Bank and the microfinance movement, let’s find out what made him think about it? How did he come up with this self-sustainable model ‘Grameen’ for micro lending?[/vc_column_text][/vc_column_inner][vc_column_inner width=”1/3″][vc_column_text]

Prof.Muhammad Yunus

[/vc_column_text][vc_empty_space][/vc_column_inner][/vc_row_inner][vc_column_text]

[/vc_column_text][vc_empty_space][/vc_column][/vc_row][vc_row full_width=”stretch_row” el_id=”chapter3″ css=”.vc_custom_1504721283256{background-color: #002e4b !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading source=”” text=”Chapter 3:

The Story of Microfinance” link=”” font_container=”tag:h1|text_align:center|color:%23ffffff” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:300%20light%20regular%3A300%3Anormal” el_class=”chapter_head” css=”” icon=”” icon_size=”” subtitle=””][vc_empty_space height=”16px”][vc_column_text]In the last chapter, I specified that the microfinance movement led to the rise of SHGs. But, how exactly did the microfinance movement emerge in the first place? Who concocted it? Here’s a short story about the history of microfinance industry.[/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]The Bangladesh Famine of 1974 inspired him to do something for the eradication of poverty. From his research and personal experiences, Muhammad Yunus found that small loans could make a great deal of difference in the life of a underprivileged person. But the traditional banking models leered at his theory.

Muhammad Yunus was bothered by the anti-poor, money-minded, anti-social conscious, anti-women, and money minded mentality of traditional banks. To bridge the burgeoning poverty gap and maintain the status quo between the rich and the poor, he started the microfinance movement.

He did not have a business plan or approach drawn out. He stood strong in his stance that the poor were credit-worthy and trustworthy. He aspired to break the stereotypical way of lending. In order to achieve that feet, he decided to do the exact opposite of what a conventional bank did.

Banks lent to men; he extended credits to women. Financial Institutions demanded collateral; he offered collateral-free loans. The traditional lenders set their prime focus on urban areas or cities; he reached out to rural and remote areas.

[/vc_column_text][vc_row_inner][vc_column_inner width=”2/3″][vc_column_text]He believed credit is a fundamental human right and offering the poor a loan instead of charity eventually changed their way of life and sparked the sense of entrepreneurship hidden within them. Instead of offering the poor fish (money/charity) to alleviate their hunger, he taught them how to fish (make money).

So, instead of offering them donations or charity, he offered the struggling folks a loan to create self-employment opportunities with a credit which helped them generate income for themselves so that they could take care of their right to food, right to shelter with their own hard work. This eventually led to the formation of “Grameen Bank.”[/vc_column_text][vc_empty_space height=”24px”][/vc_column_inner][vc_column_inner width=”1/3″][vc_empty_space height=”24px”][vc_column_text]

When the banks thought the wealthy and affluent made better borrowers, he proved that the poor were not only reliable borrowers but were also astute entrepreneurs.

[/vc_column_text][vc_empty_space height=”28px”][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]

[/vc_column_text][vc_empty_space][/vc_column][/vc_row][vc_row full_width=”stretch_row” el_id=”chapter4″ css=”.vc_custom_1504722009214{background-color: #002e4b !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading source=”” text=”Chapter 4:

Grameen Bank” link=”” font_container=”tag:h1|text_align:center|color:%23ffffff” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:300%20light%20regular%3A300%3Anormal” el_class=”chapter_head” css=”” icon=”” icon_size=”” subtitle=””][/vc_column_inner][/vc_row_inner][vc_empty_space height=”16px”][vc_column_text]In the previous chapter, we got to know a bit about the founder of the Grameen Bank and the reason why it was formed. Here’s a short chapter dedicated to the revolutionary model of microfinance which was established amidst several controversial opinions which predicted its gloom and doom. [/vc_column_text][vc_empty_space height=”10px”][/vc_column][/vc_row][vc_row][vc_column width=”1/2″][vc_empty_space][vc_column_text]Grameen Bank (Grameen means “Rural or Village” Bank in Bengali) was originated in 1976 as an innovative rural banking programme which was committed to provide the rural poor credit and banking services and help them snap out of the poverty ridden state.

Grameen offered the poorest of the poor micro credits or grameen credit without any collaterals. Grameen destroyed the myth about lending to the poor being a risky business by exhibiting a stable 98% repayment rate over the last two decades by lending out a sum of approximately 6.5 billion dollars to the impoverished.[/vc_column_text][/vc_column][vc_column width=”1/2″][vc_empty_space][vc_column_text] [/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]

[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]

[/vc_column_text][vc_empty_space][/vc_column][/vc_row][vc_row full_width=”stretch_row” el_id=”chapter5″ css=”.vc_custom_1504722854610{background-color: #002e4b !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading source=”” text=”Chapter 5:

Indian Model” link=”” font_container=”tag:h1|text_align:center|color:%23ffffff” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:300%20light%20regular%3A300%3Anormal” el_class=”chapter_head” css=”” icon=”” icon_size=”” subtitle=””][vc_empty_space height=”16px”][vc_column_text]Albeit being inspired by the Bangladeshi idea, NGOs like Annapurna Mahila Mandal (in Maharashtra) ‘Working Women’s Forum’ (in Tamilnadu), Self-employed Employed Women Workers Association (in Gujarat) and the other apex institutions like National Bank for Agriculture and Rural Development (NABARD) have played a vital role in establishing the SHG concept in India.

Here’s a brief timeline of the important milestones in the journey of SHG. A quick look at the evolution of SHG model in India.[/vc_column_text][/vc_column_inner][/vc_row_inner][vc_empty_space height=”16px”][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][stm_company_history][stm_company_history_item year=”1984-1985″ title=”MYRADA” description=”MYRADA, an NGO started the first SHG in the period 1984-1985. This Karnataka based NGO encouraged the rural women to form local groups to secure collective credit and educated them on how to use their savings towards achieving economically profitable employment. “][stm_company_history_item year=”1986-1987″ title=”Research Project by NABARD” description=”NABARD funded a research project on “Savings and Credit Management of Self Help Groups” of Mysore Resettlement and Development Agency (MYRADA) during the year of 1986-87. This aspect caused a spike of interest in the Group lending prospect.”][stm_company_history_item year=”1988-1989″ title=”Survey” description=”Following the research project, NABARD took an official survey of 43 NGOs spread over 11 states in India to investigate the possibilities of collaborating SHGs with Banks to raise the rural savings and extend a line of credit to the poor.”][stm_company_history_item year=”1991-1992″ title=”Pilot Project” description=”Enlightened by the results obtained from the survey, NABARD recommended RBI to advise the Banks to extend credit to the list of 500 SHGs which were under NABARD’s pilot project in 1991-92. NABARD started encouraging self-help groups on a large scale from the period 1991-92.”][stm_company_history_item year=”1993″ title=”RBI Circular” description=”RBI permitted SHGs to have a savings account in banks from the year of 1993. This action gave a considerable boost to the SHG movement and paved the way for the SHG-Bank linkage program. “][stm_company_history_item year=”1994″ title=”Working Group” description=”After getting to know the hidden potential of SHGs RBI constituted a group in Nov 1994 to review the functionalities of NGOs & SHGs and make appropriate recommendations to expand their activities further and deepen their role in rural development.”][stm_company_history_item year=”1996″ title=”Policy Change” description=”SHGs became a regular component of the Indian Financial System this year. RBI started implementing process of offering microfinance as one of its major policies.”][/stm_company_history][vc_empty_space][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]

[/vc_column_text][vc_empty_space][/vc_column][/vc_row][vc_row full_width=”stretch_row” el_id=”chapter6″ css=”.vc_custom_1504755291043{background-color: #002e4b !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading source=”” text=”Chapter 6:

Concept of SHGs” link=”” font_container=”tag:h1|text_align:center|color:%23ffffff” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:300%20light%20regular%3A300%3Anormal” el_class=”chapter_head” css=”” icon=”” icon_size=”” subtitle=””][/vc_column_inner][/vc_row_inner][vc_empty_space height=”16px”][vc_column_text]Now that we got to know the history behind SHGs let’s get right to their concept. How do they work? What is their main objective?

SHGs are small (with 10-20 members) homogenous (primarily made up of only women) groups which are formed voluntarily (with the help of an external agency) and follow the mandatory requirements given below[/vc_column_text][vc_empty_space height=”16px”][/vc_column][/vc_row][vc_row][vc_column width=”1/2″][vc_empty_space][vc_empty_space][vc_column_text]

Discipline

The group is expected to create a code of conduct (norms for the management). Each member should abide by those norms and take part in the frequent meetings (every week or every fortnight) at a pre-designated place. All members are expected to be present at the meeting. This aspect is intended to test the discipline of the Group members. The group ought to come up with an agenda for each meeting and organize discussions as per the agenda.

Unity

The group should elect an animator and a representative to unanimously lead the Group. All group activities are expected to be conducted democratically right from choosing a leader to exchange views during a meeting, and all members are encouraged to take part in the decision-making process actively. This intends to ingrain the vote of unity among the Group members.

Savings

Members must agree to make the regular contribution to the fund pool. Every member ought to save at least 100 INR per month at least for 6 months. This rule is present to test the patience of the Group members and instill a sense of mutual trust and connection among the members. Once they make a decent saving, the Group could internally lend the amount to its member for consumption or income generation purposes.

Support

Though there are a large number of members, the resource available might be comparatively small, and so a group would not be able to lend to all its members. At this point, the group has to take measures for prioritizing the application of a person with absolute need by analyzing their purpose and endowment level. A fair discussion removes all sense of favoritism, helps the Group identify the right borrower and also instills a sense of responsibility within the borrower.

Repayment

The group should also decide upon the norms for loans which cover all the aspect of the loan sanction procedure including repayment schedule and interest rates etc. All loans are offered based on the collective decision taken by the group with the terms that were sketched out earlier. The animator and representative are expected to closely monitor repayments from the loanee and make a note of delinquency or arrears (if any).[/vc_column_text][/vc_column][vc_column width=”1/2″][vc_empty_space][vc_single_image image=”16005″ img_size=”full” alignment=”center”][/vc_column][/vc_row][vc_row][vc_column][vc_column_text]

Bookkeeping

As a part of bookkeeping SHGs must maintain a list of mandatory records such as admission register, attendance register, general ledger with the account of savings made, loan ledger, Bank Passbook, Individual Passbook of members and Cash book. Maintaining these records would inject transparency into the working of SHG, and also these records help banks, financial institutions, and NGOs get a better understanding of the progress of SHG.

You May Also Like: CloudBankIN – Saas Banking Engine

Bank Loan

After showing consistent progress for a minimum period of 6 months, the SHGs become eligible to approach the bank requesting a loan with a genuine reason for the credit demand, proofs for the credit handling capacity of Group member, the records maintained till date, the accounting procedure, etc.. The bank would then extend to the Group depending on the documents submitted.

Key Binders

The group members are jointly accountable for the repayment of bank loan. This aspect provides the group member the necessary incentive to monitor and enforce the responsibility to repay the loan borrowed promptly. Three elements namely the peer-pressure, mutual accountability and the collective decision making remain to be the most important defenses for the banks to do business with the poor and informal group of women situated in the rural area.[/vc_column_text][vc_empty_space][vc_column_text]

[/vc_column_text][vc_empty_space][/vc_column][/vc_row][vc_row full_width=”stretch_row” el_id=”chapter7″ css=”.vc_custom_1504756433658{background-color: #002e4b !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading source=”” text=”Chapter 7:

Role of Promotional Institutions” link=”” font_container=”tag:h1|text_align:center|color:%23ffffff” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:300%20light%20regular%3A300%3Anormal” el_class=”chapter_head” css=”” icon=”” icon_size=”” subtitle=””][/vc_column_inner][/vc_row_inner][vc_empty_space height=”16px”][vc_column_text]I can hear you guys say “What are Promotional Institutions?” What have they got to do with SHGs? Let me start explaining before you folks start fretting.

Institutions such as MFIs, NBFC, Banks, NGOs, Cooperative Societies and other financial or non-profit institutions could either reach other through field officers or Business Correspondents help individuals in the rural area to form a JLG and rise loan for income generating activities. I decided to label them promotional institutions just for the ease of it.

Let’s see in detail how these Institutions and its representatives play a crucial role in ensuring the economic prosperity of our nation with women empowerment through SHGs. [/vc_column_text][vc_empty_space height=”16px”][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]They aspire to harness the potential hidden within the rural roots of our country through a slew of financial services aimed at bringing about changes in the living conditions of the downtrodden women.

The Representatives are associated with SHGs right from the grassroots level enabling the formation and promotion of SHGs and creating a credit linkage system with major stakeholders like banks and other financial institutions to kick start economic activities.

In order to get a better understanding of the commitment of these promotional institutions and their representatives towards nurturing SHGs, we could take a look at the SHG development cycle:

- Collect necessary information about the Village before visit and analyze its credit needs, the primary sources of income, the skill set of workers, a comprehensive review of available natural and social resources, etc.

- Once the analysis is complete, the field officers meet the women in the village directly or through the administrative officers to explain them the purpose of their intervention and create awareness about the SHG concept. The field officers would then spread out the information, prep and encourage the women in the village to form SHGs.

[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column width=”1/2″][vc_empty_space height=”16px”][vc_column_text]

- After spurring the scope for interest among the women making them agree to form SHGs, the field officers then help them organize the groups, decide upon a name, draft the rules and regulations for managing groups, help them select leaders and open a bank account for savings.

- During the first few meetings, representatives would advise the elected leaders how to organize a meeting, setting an agenda for each meeting, help them sketch out a plan as to what ought to be discussed, get them familiarized with the books that need to be maintained, how to go about initiating internal loans from the savings, etc.

- Over the next few months, the representatives would organize special training sessions for SHGs to develop the skill set of Group members enabling them to utilize the loans efficiently and help them identify income generating ideas.

- Apart from emphasizing the importance of savings and internal lending, the Representatives also encourage the SHGs to take part in a common action program such as tree plantation, cleaning the streets, health camps, building a water source etc.. The representatives plan with the villagers and help them organise it.

[/vc_column_text][/vc_column][vc_column width=”1/2″][vc_empty_space height=”40px”][vc_single_image image=”16236″ img_size=”full” alignment=”center”][vc_column_text]

Source: Insidehighered

[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space height=”24px”][vc_column_text]

- After the completion of a 6-month period, the field officers would bring in bankers or government officials to interact with the members of SHGs to analyze their credit-worthiness, test their consistency and performance before offering a loan for income generation purpose. This process is called Grading. Based on the grade they get, the loan application of the SHGs may be accepted or rejected.

- As SHGs take active participation in the income generation activities turning to a micro enterprise, their products are services are required to be monitored effectively to promote the income of SHG members. The Field Agents shoulder the responsibility to show them the ropes of how to market their products as well.

You May Also Like: Why Should You Use A Cloud-Based Loan Management Software?

The promotional institutions and their field officers will guide and nurture the SHGs for almost 36 months from the date of their inception.

These institutions play a crucial role in the process of formation, progression, and strengthening of SHGs in turning them into self-sustainable institutions which are capable of withstanding the democratic phases of development.[/vc_column_text][vc_column_text]

[/vc_column_text][vc_empty_space][/vc_column][/vc_row][vc_row full_width=”stretch_row” el_id=”chapter8″ css=”.vc_custom_1504757520108{background-color: #002e4b !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading source=”” text=”Chapter 8:

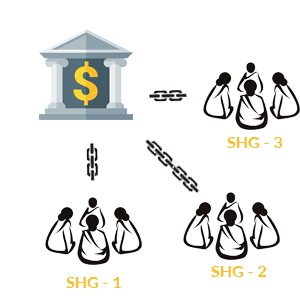

SHG Bank Linkage Program” link=”” font_container=”tag:h1|text_align:center|color:%23ffffff” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:300%20light%20regular%3A300%3Anormal” el_class=”chapter_head” css=”” icon=”” icon_size=”” subtitle=””][/vc_column_inner][/vc_row_inner][vc_empty_space height=”16px”][vc_column_text]We all know that the SHG Bank linkage program was sactioned after the positive results showcased by MYRADA project. How exactly does it work? What factors do banks or other financial institutions take into consideration before offering the SHGs a loan? Before that let’s start with a brief history of the SHG Bank Linkage model :)[/vc_column_text][vc_empty_space height=”16px”][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]The SHG – Bank Linkage Program was sanctioned due to the positive results that were shown by the MYRADA project in 1989. A credit of INR 10 lakh was authorized to experiment with credit management groups. The program was formally launched during the pilot project phase in 1991-1992 where 500 SHGs were linked with banks.

SHG Bank linkage program was initially sketched as a partnership model between three agencies namely NABARD, Banks and the NGOs. This pilot version of bank linkage program was later on streamlined after RBI’s approval enabling SHGs to open bank accounts.

Below this program, banks started extending loans to SHGs against their savings and the group guarantee. The loan Quantum’s offered could be as large as three times that of the amount saved by SHGs in their account.

[/vc_column_text][vc_column_text]Before providing loans to SHGs banks tend to take the credit requirement of the SHGs into consideration namely

- Is the loan used for income generation activity?

- Is the member going to use this loan for social needs like housing, marriage, etc.?

[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column width=”1/2″][vc_empty_space][vc_column_text]Though banks tend to accept reasons like debt swapping, consumption, etc.. the above two cases seem to receive maximum priority.

Once banks approve the loan application of SHGs, the amount would be disbursed to the group’s account. This would then be collected and distributed among the Group members by the animator and representative.

However, this process of disbursement led to a few complicated situations where the funds were embezzled by the field officers, animators or representatives. In order to resolve this problem, the banks came up with the plan of creating individual accounts for each member of the Group.

Following this concept, the loan amount is now disbursed directly to the respective accounts of Group members. In addition to preventing frauds and other virulent operations, this procedure has also injected a sense of much-needed transparency in the disbursal phase.

In RBI’s recent guidelines for Priority Sector Lending, SHGs are made eligible to be categorized under as priority sector advance below their respective categories namely Agriculture, Small / Medium / Micro Enterprises, and ‘Others.’

Did you know that there are over 85,76,875 savings linked Self Help Groups with approximately 16,114 Crores savings in India? Isn’t it mind blowing? Who knew there were more than 85 lakh Self Help Groups in India?[/vc_column_text][/vc_column][vc_column width=”1/2″][vc_empty_space][vc_single_image image=”7134″ img_size=”full” alignment=”center”][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]What’s curious is that, out of these 85 lakh groups, only 18,98,120 are credit linked with Banks. That’s approximately 22%! Why is it so? Before we delve deeper into the numbers in search of an answer, let’s looking closely at the social and economic impact of SHGs in India.[/vc_column_text][vc_column_text]

[/vc_column_text][vc_empty_space][/vc_column][/vc_row][vc_row full_width=”stretch_row” el_id=”chapter9″ css=”.vc_custom_1504758195866{background-color: #002e4b !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading source=”” text=”Chapter 9:

Long-term Socio-economic impact of SHGs” link=”” font_container=”tag:h1|text_align:center|color:%23ffffff” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:300%20light%20regular%3A300%3Anormal” el_class=”chapter_head” css=”” icon=”” icon_size=”” subtitle=””][/vc_column_inner][/vc_row_inner][vc_empty_space height=”16px”][vc_column_text]India has been a predominantly gender-biased society where the women have fallen prey to the discrimination tactics and have started accepting it subserviently. SHG’s have provided the rural women with a much-needed boost in self-confidence and encouraged them to become more self-reliant.[/vc_column_text][vc_empty_space height=”16px”][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space height=”16px”][vc_column_text]

Social Impact:

Even today, several women in rural areas are disrespected, oppressed, sidelined, humiliated, exploited, and kept away from their fundamental rights.

The confidence and self-respect the SHGs imbibed in rural women through the training regime and credit programs have helped them break out of the chains of domestic slavery and emerge as self-reliant charismatic women who are capable of conquering the world.

The following are some of the significant social impacts made by SHGs:[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column width=”1/2″][vc_empty_space height=”16px”][vc_column_text]

- Emancipates women from the vicious male dominance

- Enhances the social status and respect for women

- Alleviates domestic violence, verbal abuse and alcoholism

- Eradicates social evils like Female Infanticide, Caste discrimination, etc

- Improves the Livelihood of people in rural areas

- Improvement in the enrollment and retention rate of girls in educational institutions

- Enables women to influence the decision making process within household and communities

[/vc_column_text][/vc_column][vc_column width=”1/2″][vc_single_image image=”16231″ img_size=”medium” alignment=”center”][vc_column_text]

Source: The Indian Society

[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]

Economic Impact:

The Social mobility aspect encouraged by SHGs ensures that the society steers clear of the pathological condition of social decaying due to illiteracy, and ignorance. It promotes the formation of micro-enterprises to facilitate eradication of poverty through income generation and employment opportunities. Here are the significant economic empowerment changes made by the SHGs:

- Encouraging the spirit of entrepreneurship by offering income generation loans

- Alleviating poverty through income generation and employment opportunities

- Micro-enterprises act as a catalyst for the formation of social capital in the Nation

- Addressing the existing problems in a community like drinking water issues, and serve as the ‘face of development’ to resolve them

- Taking the initiative to organize social upliftment activities such as village cleaning drives, installing community taps, organizing a protest to remove liquor shops located near schools, religious places, etc.

[/vc_column_text][vc_column_text]

[/vc_column_text][vc_empty_space][/vc_column][/vc_row][vc_row full_width=”stretch_row” el_id=”chapter10″ css=”.vc_custom_1504760423045{background-color: #002e4b !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading source=”” text=”Chapter 10:

SHG vs JLG” link=”” font_container=”tag:h1|text_align:center|color:%23ffffff” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:300%20light%20regular%3A300%3Anormal” el_class=”chapter_head” css=”” icon=”” icon_size=”” subtitle=””][/vc_column_inner][/vc_row_inner][vc_empty_space height=”16px”][vc_column_text]Folks tend to use SHG and JLG interchangeably without a clue that they are two entirely different things. I used to be one of those clueless people who used to mix-up both these concepts. However, a bit of research I was able to understand the little nuances that differentiated these two group loan models. Here’s what I garnered outta my investigation.[/vc_column_text][vc_empty_space height=”16px”][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]

SHGs

SHGs are primarily savings oriented. Though they are formed with the intention to offer women economic independence, the main aspect of this group is to imbibe a strong saving mentality among rural women. The amount of loan value offered to the group depends on the total amount of savings. Financial institutions may offer upto 3 times the amount of saving made by the Group.

You May Also Like: How Fintech Is Transforming Microfinance institution in Australia

JLGs

JLGs on the other hand, are primarily credit based model. Borrowers from the same social economic background form groups seeking loan for income-generation purposes. Though JLG are credit oriented model, the members are often encouraged to open a ”No Frills Account” individually.

The decision is entirely that of the JLG members. If a JLG decides to undertake savings as well, they would just have to initiate a savings account and start maintaining the appropriate book of accounts. However, this savings amount would not impact the loan process in anyway. The loan would be processed based on credit assessment of the Group which would be depend completely on the income generation activities and the credit-need of the individual members.

That’s just a short overview of the models. Please refer the image representation to know more 🙂

[/vc_column_text][vc_row_inner][vc_column_inner][vc_single_image image=”16003″ img_size=”full” alignment=”center”][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]

[/vc_column_text][vc_empty_space][/vc_column][/vc_row][vc_row full_width=”stretch_row” el_id=”chapter11″ css=”.vc_custom_1504761768644{background-color: #002e4b !important;}”][vc_column][vc_row_inner][vc_column_inner][vc_custom_heading source=”” text=”Chapter 11:

Current Scenario” link=”” font_container=”tag:h1|text_align:center|color:%23ffffff” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:300%20light%20regular%3A300%3Anormal” el_class=”chapter_head” css=”” icon=”” icon_size=”” subtitle=””][/vc_column_inner][/vc_row_inner][vc_empty_space height=”16px”][vc_column_text]

Today, SHGs have started addressing the multidimensional aspects of poverty holistically. Being an active participation program, it is the women themselves who are influencing the direction of the training and ensure the success of an SHG program.

How has the SHG program evolved so far? What sectors have been impacted by their contribution? How are the financial institutions helping SHGs sustain? Is the Government supporting and promoting the self-help group movement? Keep reading to know more.[/vc_column_text][vc_empty_space][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_row_inner][vc_column_inner width=”1/2″][vc_column_text]With the new surge of confidence and awareness ingrained through the SHG training, there has been a vast improvement in their involvement with regards to health, education and several social sectors. In addition to this, the mobility of women in public domain has increased remarkably.

The development of Micro-enterprises has been adopted widely as an anti-poverty strategy in most of the developing countries. Micro enterprises have become a powerhouse of economic growth and equitable expansion of the country.

The SHGs have bridged several gaps in the caste system, the male dominance and domestic violence have declined at an impressive rate owing to measures carried out for gender-equality. There have been changes in the constitution as well, the panchayat raj system which offered 50% seats to women candidates is a whopping step towards creating an anti-biased inclusive nation.

SHG owned businesses are the fastest growing divisions of the micro enterprise industry as the support program strives to offer people a few modest means to kick start their entrepreneurship journey. From being presented with the opportunity to manage a major tourist destination for the first time to manufacturing unique products which win accolades for their exceptional quality. [/vc_column_text][/vc_column_inner][vc_column_inner width=”1/2″][vc_empty_space height=”48px”][vc_column_text]

Source: Telangana Today

Stree Nidhi Credit Cooperative Federation (A State Level Apex Society) unveiled a massive annual credit plan of Rs 1,810 Crfor the financial year 2017-18 jointly with Federation of Self-Help Groups (SHGs) and the State government.[/vc_column_text][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]SHGs have become a new identity of the rural economy and even the Governing bodies have understood the importance of nourishing these little rays of sunshine. While the state governments are taking measures to scale up the operations of SHG by digitizing them, the central government, on the other hand, has resorted to allocated more funds for the development of SHGs.

This active involvement showed by the government has made the SHG model an indigenous way to reach out the poor and create a poverty-free world.[/vc_column_text][vc_column_text]

[/vc_column_text][vc_empty_space][/vc_column][/vc_row][vc_row full_width=”stretch_row” el_id=”chapter12″ css=”.vc_custom_1504763118472{background-color: #002e4b !important;}”][vc_column][vc_custom_heading source=”” text=”Chapter 12:

Summary” link=”” font_container=”tag:h1|text_align:center|color:%23ffffff” use_theme_fonts=”yes” google_fonts=”font_family:Open%20Sans%3A300%2C300italic%2Cregular%2Citalic%2C600%2C600italic%2C700%2C700italic%2C800%2C800italic|font_style:300%20light%20regular%3A300%3Anormal” el_class=”chapter_head” css=”” icon=”” icon_size=”” subtitle=””][vc_empty_space height=”16px”][vc_column_text]I can hear a few voices call out to me saying, “Whats gonna be different in your summary? It’s just gotta be the same ‘rose-tinted view’ of SHGs nah!” Nope, not really. Yes, I did describe an ideal SHG in my article. But, even this scenario is not completely flawless.

Like every other model of finance, the present SHG model has its own shortcomings despite the monumental support it receives. What is it? Aren’t you curious??[/vc_column_text][vc_empty_space height=”16px”][/vc_column][/vc_row][vc_row][vc_column][vc_empty_space][vc_column_text]It is true, SHGs have played a significant role in promoting gender-equality, economic independence, political participation, shared responsibility, and social development. However, they have a long way to go when we look at their entrepreneurial journey.

When we take an attempt to look beyond the empowerment mantra, we’d be able to decipher the struggle for self-sustenance in the micro enterprise sector. While the support offered by NABARD, Government, and banks has kept the SHG movement going, it’s time to spend more effort on smoothing the implementation issues that arise out of sharp procedures followed by Lending Institutions.

Researchers seem to denote that micro-enterprises are having a hard time sustaining due to an insufficient generation of income. Micro-enterprises are sometimes criticized to be exploiting women and children. These comments are often by said people who fail to see how they improve the livelihood of rural areas.

The lack of marketing strategies, problem obtaining good quality raw material, inconsistent quality and lack of insight about the market seems to be the major reason for failures of micro enterprises.

For scaling up micro enterprises, organizations should dovetail entrepreneurship development programs at district levels to upgrade skill set and market knowledge of the budding micro-entrepreneurs.

Revamping the training program by offering field visits to successful SHG units, providing quality raw material at affordable cost, ensuring the availability of adequate and timely credit would streamline the growth of micro enterprises and SHGs.

Let me conclude this by saying that just marginalizing the poor & offering them a means to start a business would not suffice. To make the SHGs a driving force behind social upliftment and economic development through entrepreneurship, the government and financial institutions need to take a proactive role in offering them technical expertise to survive the cutting-edge competition.

Backed by appropriate institutional support, the SHGs could completely break the barriers which prevent them from making a significant economic contribution through productive and sustainable income generating activities. Well, that’s my humble opinion. Your perspective may differ from mine. [/vc_column_text][vc_column_text]

So, what do you think?

Is the credit extended for SHGs sufficient to help them create their own niche? Are SHGs really empowering women and contributing to the development of a harmonious nation? Does the aspect of addressing the skill set gap really help the SHG led micro enterprises to persevere in the trials of business? Feel free to share your thoughts in the comment section :)[/vc_column_text][vc_column_text]

[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][stm_post_comments][vc_column_text]

Most Recent Posts

[/vc_column_text][/vc_column][/vc_row]